In 2023, gross disposable income per capita increased compared to 2019, exceeding pre-pandemic levels. The latest available data highlights that in 2021 the average family income began to grow again both in nominal and real terms. The net income inequality index also improves, while the population at risk of poverty remains substantially stable compared to the previous three years.

This is the new photograph taken byIstat in the eleventh edition of Bes-Report on fair and sustainable well-being. The 2024 Report analyzes 12 different macro-sectors: Health; Education and training; Work and life balance; Economic well-being; Social relations; Politics and institutions; Safety; Subjective well-being; Landscape and cultural heritage; Environment; Innovation, research and creativity; Quality of services.

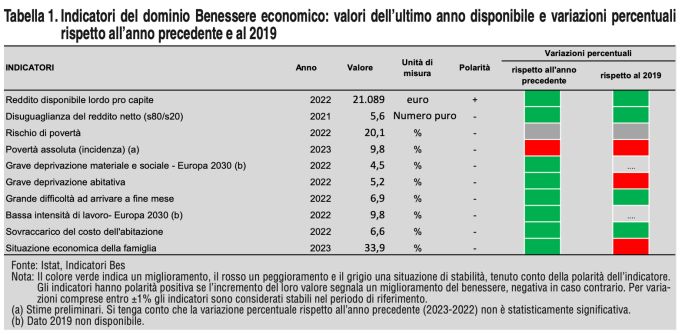

Let’s see what emerges regarding economic well-being.

The Italian economy in 2023

According to Istat’s Bes 2024 Report, in 2023, theItalian economy recorded one growth of 0.9%in decrease compared to 2022 of 4%. Growth was mainly supported by domestic demand, with consumption and investment in equal measure. On the supply side of goods and services, added value has led to an increase in the construction sector and in many tertiary sectors, while it has suffered a contraction in agriculture and overall mining, manufacturing and industry in general.

The framework tells us that, basically, things in Italy have improved compared to the previous year and, in some cases, also compared to 2019. The only exception is the absolute poverty indicatorwhich worsens compared to the pre-pandemic situation, although it remains substantially stable between 2022 and 2023. The cause is essentially inflation, which has generated a significant loss in families’ purchasing power.

Income data

In 2023, the gross disposable income per capita (i.e. the ratio between the gross disposable income of consumer families and the total number of resident people) increased by 14.9% compared to 2019, exceeding pre-pandemic levels. The latest available data highlights that in 2021 the average family income, equal to 33,798 eurosbegan to grow again both in nominal terms (+3%) and in real terms (+1%).

It also improves thenet income inequality index (i.e. the ratio between the total equivalent income received by the 20% of the population with the highest income and that received by the 20% of the population with the lowest income), which has a value of 5.6, decreasing compared to the previous year (it was 5.9 in 2020) and slightly lower than the pre-Covid period, when it was 5.7. It remains substantially stable compared to the three years preceding the population at risk of povertyequal to 20.1% in 2022.

In the first quarter 2023 the gross disposable income of families increased by 2.2% in nominal terms and by 2.1% in real terms, affected only marginally by the increase in prices, while final consumption expenditure grew in nominal terms by ‘1.0%. The propensity to save of families marked the first increase of 1.1% compared to the previous quarter, after several quarters of decrease, settling at 6.4%.

In the second trimester iincome decreased by 0.5% compared to the previous quarter, while consumption grew by 0.3%. The increase in final consumption spending is reflected in a decline in the propensity to save which, having already been below pre-Covid levels for several quarters, fell by 0.7% compared to the previous quarter, reaching 5.7%.

In the third quarter, income increased by 1.7% compared to the previous quarter, while consumption grew by 1.3%. The purchasing power of families, after the sharp fall in the fourth quarter of 2022, continues to recover, increasing by 1.1% compared to the previous quarter. The recovery, which began in the first quarter of 2023, was interrupted by the slight decline in the following quarter. The trend in the propensity to save was also similar, equal to 6.1%, up 0.4 percentage points compared to the previous quarter.

The fourth quarter 2023 is the turning point, because the long sequence of negative variations in the propensity to save is finally interrupted, as many as 10, reaching 7%. Purchasing power decreased by 0.5% compared to the previous quarter, however recording the first positive sign in trend terms since the first quarter of 2022. Both the propensity to save and purchasing power, however, remain significantly lower of pre-Covid levels.

Data on the condition of severe deprivation

As the economy recovers after the sharp contraction of 2020, the population in conditions of serious material and social deprivation is significantly reduced.

Severe material and social deprivation refers to the percentage of people in families experiencing it at least 7 of these 13 conditions: not being able to pay unexpected expenses; not being able to afford a week’s holiday a year away from home; being in arrears on bills, rent, mortgage or other loans; not being able to afford an adequate meal at least once every two days, i.e. with proteins from meat, fish or equivalent vegetarian; not being able to adequately heat the home; not being able to afford a car; not being able to replace damaged or out-of-use furniture with others in good condition; not being able to afford a usable internet connection at home; not being able to replace old clothes with new ones; not being able to afford two pairs of shoes in good condition every day; not being able to afford to spend a small sum of money on personal needs almost every week; not being able to afford to regularly carry out paid leisure activities outside the home; and finally to meet family or friends to drink or eat together at least once a month.

In 2022 in Italy they find themselves in conditions of material and social deprivation 4.5% of individuals, compared to one European average of 6.7%.

Among the European Union countries, Romania (24.3%) and Bulgaria (18.7%) record the highest values of the indicator, distancing themselves considerably from the other countries. Greece follows, which stands at around 14%. Slovenia and Finland, on the other hand, are virtuous, where the share of people living in a condition of material and social deprivation is very low, even below 2%.

The number of people living in families with low work intensity is also decreasing (percentage of people living in families for which the ratio between the total number of months worked by family members and the total number of months theoretically available for work activities is less than 0.20): 9.8% compared to 10 .8% of 2021.

And the number of those is also decreasing in conditions of severe housing deprivation (percentage of people who live in overcrowded homes and who have structural problems in the home, or who do not have a bathroom or shower with running water, who have brightness problems: the data stands at levels only slightly higher than those recorded in the pre-pandemic (5.2% compared to 5.9% in 2021 and 5.0% in 2019).

Compared to previous years, the housing cost overload indicator also decreases (percentage of people living in families where the total cost of the home in which they live represents more than 40% of the net family income), which is difficult for 6.6% of the population to sustain (it was 7.2% in 2021 and 8.7% in 2019).

The most evident Istat data contained in the BES 2024 is that, in the absence of family support measuressuch as aid given during the Covid emergency and pandemic phase and the Citizenship Income, the inequality index would have been equal to 6.4a value much higher than that observed.

Data on absolute poverty

The data on absolute poverty however it does not return the same timid optimism. In fact, the value rises from 7.6% in 2019. This figure was down compared to 2018 due, in large part, to the introduction of the citizen’s income, which – recalls Istat – starting from the second quarter of 2019 approximately 1 million families had benefited.

In 2020, absolute poverty skyrocketed to 9.1%, remaining stable in 2021. In addition to the economic crisis, the decline in consumption and the spending behavior of families in the most difficult months of the pandemic had an impact.

In 2022 the incidence began to grow again, reaching 9.7%, largely due to the strong acceleration of inflation which hit less well-off families hardest. In fact, the expenditure of the latter has not managed to keep pace with the increase in prices, including that of essential goods and services considered in the basket of absolute poverty. In 2023, according to preliminary estimates, the individual incidence remains substantially stable compared to the previous year 9.8%.

The loss of purchasing power in the last 5 years

The purchasing power of Italians has suffered a collapse in the last 5 years. After a period characterized by low inflationwith an average annual variation of +0.6% in 2019 and even negative in 2020, prices experienced a sharp surge in 2021 and then in 2022. In 2022, in fact, consumer prices recorded an increase in average for the year of 8.1%, marking the largest increase since 1985, when it was +9.2%, with a peak in the fourth quarter of +11.7%.

In 2023, however, price pressures were quite limited. Over the course of the year, inflation fell rapidly, reaching 0.6% in December. In the first two months of 2024 the trend rate of change in prices remains at very moderate values, even lower than the1%.

But this slowdown did not allow the damage of the previous period to be recovered. From 2019 to 2023 the average level of the consumer price index (NIC) marks an increase of 16.2%, with notable differences between the various spending divisions. The largest variation, almost triple that recorded for the general index, is that relating to “Housing, water, electricity, gas and other fuels”, with an increase of 45%, above all due to the shock in the prices of goods energy due to the war in Ukraine.

Food products and non-alcoholic drinks were also clearly above the general index, with an increase of 22.5%; followed by Transport and Accommodation and Catering Services (+16.5% and +16.3% respectively). The rest of the sectors in the basket show increasingly smaller average variations, up to the Communications division, which recorded a drop in prices of 10.1%.

Territorial differences

Going through the map of territorial differences, we notice a strong disparity between cities. In particular, in the wake of a very long historicity, things are better in the North and Center than in the South. L’the only exception is Basilicatawhere only 21.4% declare that they have seen their economic situation worsen compared to the previous year, compared to 33.9% of the national average.

The best situation is found in Emilia-Romagna. The difference compared to other regions is more marked than the indicator of the difficulty of making ends meet. Only 1.4% of people residing in Emilia-Romagna have this problem, compared to 24.3% of those residing in Campania. The average Italian figure is 6.9%. The regions of the South, however, albeit with some exceptions, are almost always worse off. The tail light is represented precisely by Campania.

Tags: Bes Report wellbeing Italians improves average income euros

{kind=link}