France is certainly experiencing a complicated political situation, but the performance of the stock market index, rather than politics, should be explained by the often less than rational expectations of a rate cut which, in the end, did not materialise. achieved, if not in a very minimal way.

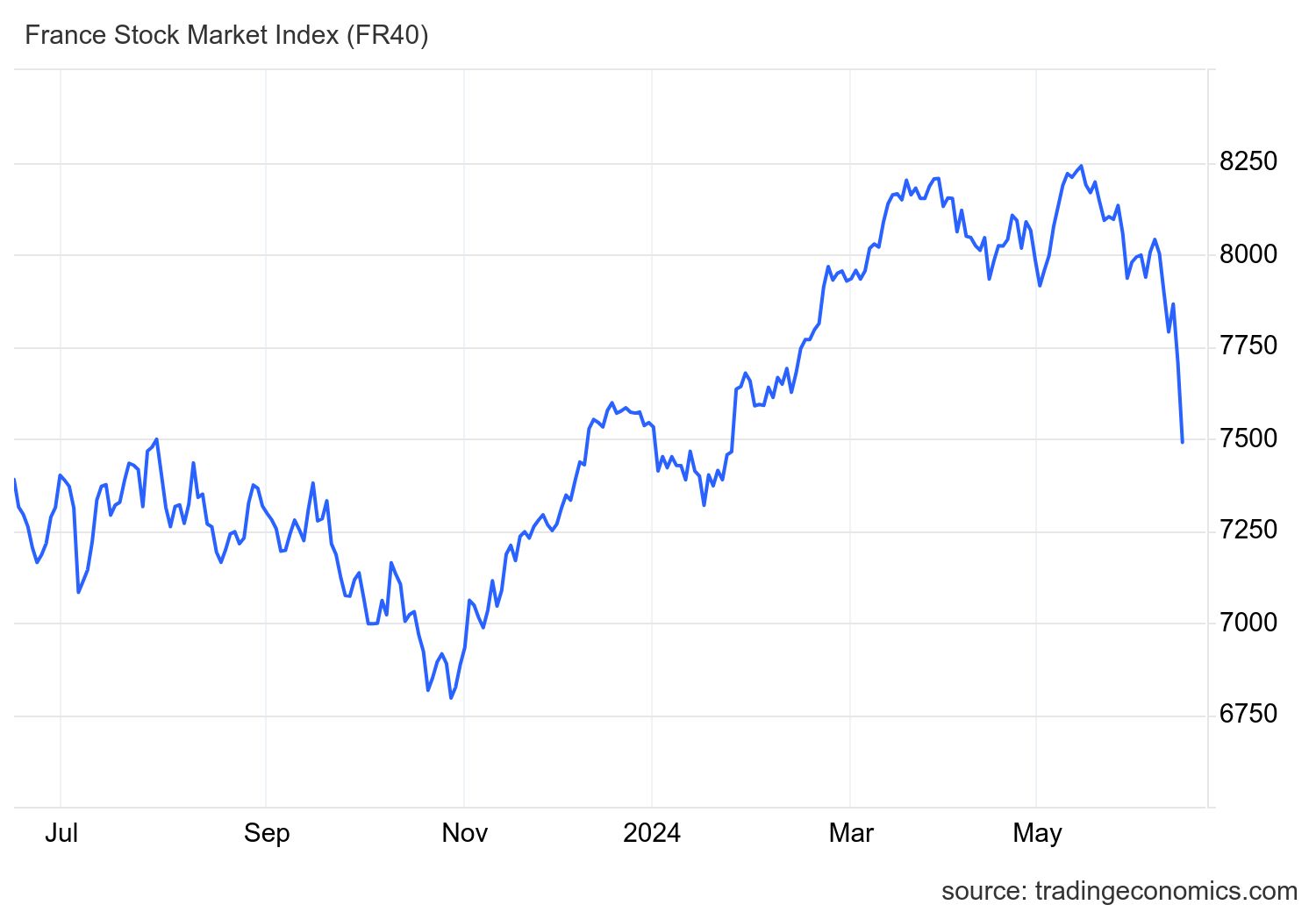

France’s blue-chip stock index, the CAC 40, fell 2.7% today and 4.6% over the past two days. Over the last six trading days, the index has lost 6.7%, and is down an incredible and staggering 8.9% from its all-time high on May 15. The trend can be seen in the graph below:

For this reason, many headlines have appeared today. The Guardian headlined: “French stock market falls on fears of far-right election victory.” The FT: “French shares suffer their worst week since 2022 due to fears of a populist victory.”

But will it really be like this? In a moderately inflationary situation in which stocks should still grow, was the news of the elections enough to make the stock market collapse? Isn’t it that the economic newspapers are moderately making fun of us or are they overestimating the political causes of the fall?

Flet’s turn to Hayek and look for the causes of a fall to the previous period, that of the boom. The CAC 40 had surged 20.7% (1,415 points) in less than seven months, from late October to its May 15 all-time high of 8,240, as a result of this epic rate-cutting mania that had also gripped Europe. So, now the ECB has cut once, and stocks are falling.

So the cause of the collapse would be linked more to expectations of a cut that did not materialize, rather than to the elections. Investors expected too much, or the ECB simply delivered too little.

The collapse was then very relative. Indeed:

- It barely erased this year’s gains. CAC is down just 0.5% year-over-year.

- It wiped out only half (737 points) of the seven-month peak of the Rate Cut Mania (1,415 points), rather than all the points plus some.

- It only brought the index back to where it was for the first time in April 2023, rather than hitting multi-year lows.

In other words, it’s not even a real sell-off, but just an 8.9% drop from record highs that were incredibly high and were based on the widespread illusion of significant rate cuts. It should be the ECB, rather than politics, that intervenes, but in this season of drugged information, everything is fine to push one’s political side.

Stock markets in general – especially in the US – have gone completely nuts in recent years, and then spectacularly during the period of rate cut anticipation, all driven by a very, very optimistic media. Now these cuts have not happened, and a scapegoat is needed. What better excuse could politics be to justify bungling finance? However, what happened in France could happen anywhere in the Euro Area at the first bad news.

Thanks to our Telegram channel you can stay updated on the publication of new Economic Scenarios articles.

⇒ Sign up right away ⇐

{kind=link}