After hitting a low point on 24 February 2024, with a price below 23 euros per MWh, gas at the Dutch TTF trading point recorded a series of increases, reaching 33 euros/MWh on 16 April. However, in the following days, the price reversed the trend, falling below 30 euros/MWh on 24 April.

As shown in Chart 1, the price increase over the last two months has affected both natural gas at the TTF and liquefied natural gas (LNG), traded at the JKM, which involves imports from Japan and South Korea.

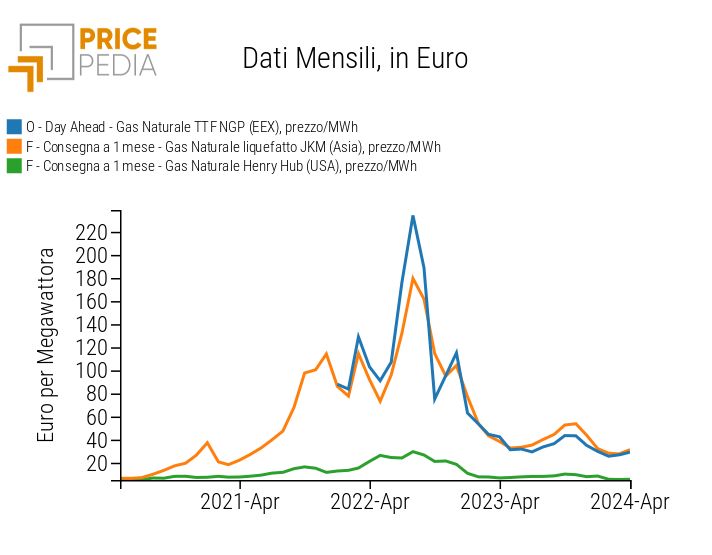

Chart 2 compares monthly prices of natural gas at TTF, LNG at JKM, and natural gas at America’s Henry Hub. This comparison highlights a strong correlation between Asian and European markets, while showing a notable difference with American prices. Therefore, it is essential to analyze the European and Asian markets and their interactions to understand the dynamics that influence TTF gas prices, which are crucial for European businesses.

Daily and monthly gas prices

| Chart 1: Daily price of gas in Europe and LNG in Asia | Chart 2: Monthly world gas prices |

To understand what is happening on the European and Asian markets, the IEA report on the world gas market in the second quarter of 2024 is particularly useful (IEA (2024), Gas Market Report, Q2-2024, IEA, Paris, License: CC BY 4.0), recently released.

- during 2023 northern hemisphere gas markets reached a new balanceafter the strong turbulence of 2021-2022;

- in the winter of 2023-2024, averagely mild temperatures were accompanied by strong cold waves which led to record-breaking peaks in demand in Northern Hemisphere markets;

- the industrial and energy sectors in the fast-growing Asian economies will lead the growth in gas consumption in 2024;

- the growth in gas consumption will be limited by theincrease in electricity production from renewable and nuclear sources;

- the effects of demand growth on prices will be limited by high levels of storage;

- The geopolitical tensions represent the greatest risk to the short-term outlook;

Strong cold waves

Despite having been an unusually mild winter on average, the 2023/24 heating season has seen several cold spells, resulting in record peaks in demand in key markets across the Northern Hemisphere.

In the United StatesWinter Storm Heather pushed natural gas consumption to an all-time high of nearly 4 billion cubic feet per day on January 16, 2024, about 30% above the December-February daily demand average.

In Europe, daily gas demand increased by almost 40% in just six days, reaching around 2.5 billion cubic meters per day in early January. The colder climate has coincided with less wind energy production, increasing demand for both space heating needs and gas demand for electricity generation.

China faced several cold waves during the 2023/24 winter season, with gas demand rising to an all-time high of 1.42 billion cubic meters per day in mid-December 2023. The cold wave caused an increase transmission pipeline utilization rates at over 90% capacity for the first time.

These events highlight the critical importance of gas supply flexibility for energy security, including in markets that are increasingly reliant on weather-sensitive renewable energy production, while using gas-fired power plants as a fallback option.

Growth in gas consumption in 2024

During the winter of 2023/24, natural gas consumption is estimated to have increased by 2%, or nearly 40 billion cubic meters, year-on-year (yoy) in the markets covered by the EIA Report. Demand growth was largely supported by increased gas use in the energy and industrial sectors, while a mild winter reduced heating needs in key Northern Hemisphere markets.

Lower prices have supported greater natural gas consumption in industrial sectors. Early estimates suggest that combined industrial gas demand in China, Europe, India and the United States, which accounts for more than half of global industrial gas consumption, increased by nearly 8% year-on-year. Industrial gas demand in Europe is showing signs of recovery with preliminary data indicating an increase of around 15% year-on-year during the 2023/24 winter, whilst remaining 10% below 2020/21 levels.

According to EIA forecasts, the demand for natural gas will increase by 2.3% in 2024, especially thanks to the rapid growth of Asian markets. The industrial and energy sectors in fast-growing Asian economies are set to drive the increase in gas consumption.

The industry is set to account for nearly 45% of global gas demand growth in 2024. This is partly driven by the expected recovery in Europe and Asian markets with price-elastic industrial demand. A significant contribution is also expected from structural growth in China and India;

More energy from renewable and nuclear sources

Natural gas consumption in Europe fell by 1% (or 3 billion cubic meters) year-on-year during the 2023/24 heating season. The mild winter climate has reduced the demand for gas in the residential and commercial sectors, but, above all, the strong expansion of renewables together with the improvement in nuclear availability has led to a reduction in the demand for gas for electricity production.

Gas consumption for electricity production is also expected to decrease by almost 10% in 2024, thanks to the improvement in the availability of nuclear power in France and the rapid expansion of renewable energy.

High levels of storage

Storage sites ended the 2023/24 heating season well above the five-year average in both Europe and the United States. The European Union ended the 2023/24 heating season with stock levels at record highs, meaning injection needs this summer could be 35% lower than the 5-year average. Lower injection demand in summer 2024 could contribute to further easing of market fundamentals.

High levels of natural gas storage are therefore expected to buffer the effects of increased demand on prices. With substantial reserves available, any sudden spikes in demand can be more easily managed without causing significant price volatility, thus ensuring market stability.

Geopolitical tensions

Geopolitical tensions pose the greatest risk to the near-term outlook. Earlier this year, maritime transport of LNG across the Red Sea was disrupted by Houthi attacks. In recent months, attacks by Russia on Ukraine’s energy infrastructure, including storage, have threatened European countries’ security of supply.

Geopolitical tensions can lead to supply disruptions, regulatory changes and unpredictable shifts in international relations. All of these factors can profoundly influence gas availability and prices on a global scale.

{kind=link}